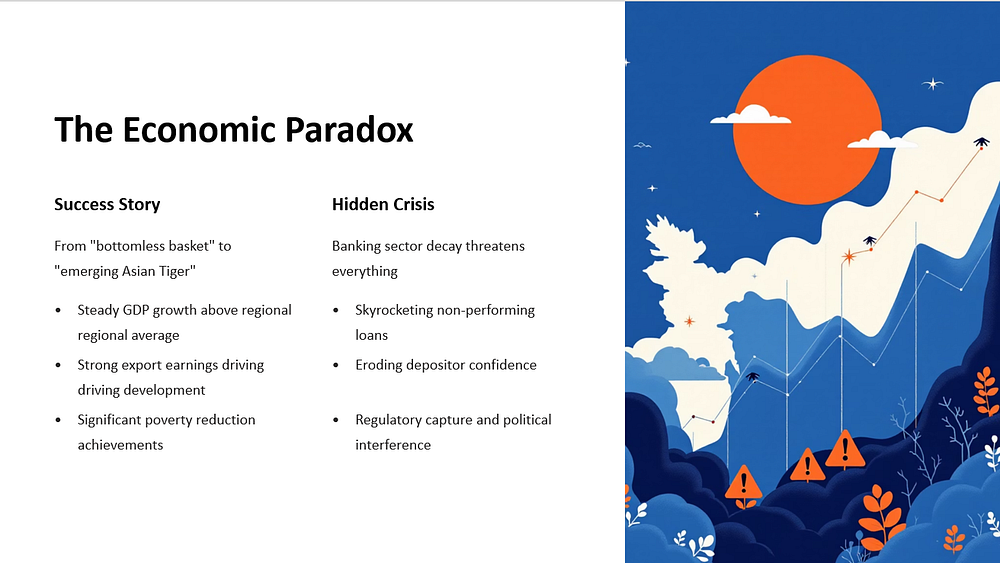

Bangladesh’s meteoric economic rise over the past two to three decades has been nothing short of impressive, worthy of countless case studies. Its transformation from being dubbed as a bottomless basket to an emerging Asian Tiger has been bolstered by steady, above-average GDP growth, export earnings, and significant poverty reduction.

However, beyond this exterior economic façade lies a severely decadent skeleton: the banking sector. The present condition of this vital sector risks eroding all that we have achieved in the past few decades due to mismanagement, rising NPL (Non-Performing Loans), poor corporate governance, weak regulatory oversight, political patronage, dominance of families in bank’s boards: resulting in a sharp erosion of public’s trust in the banking system. This crisis is real, with a drastic deterioration on the horizon.

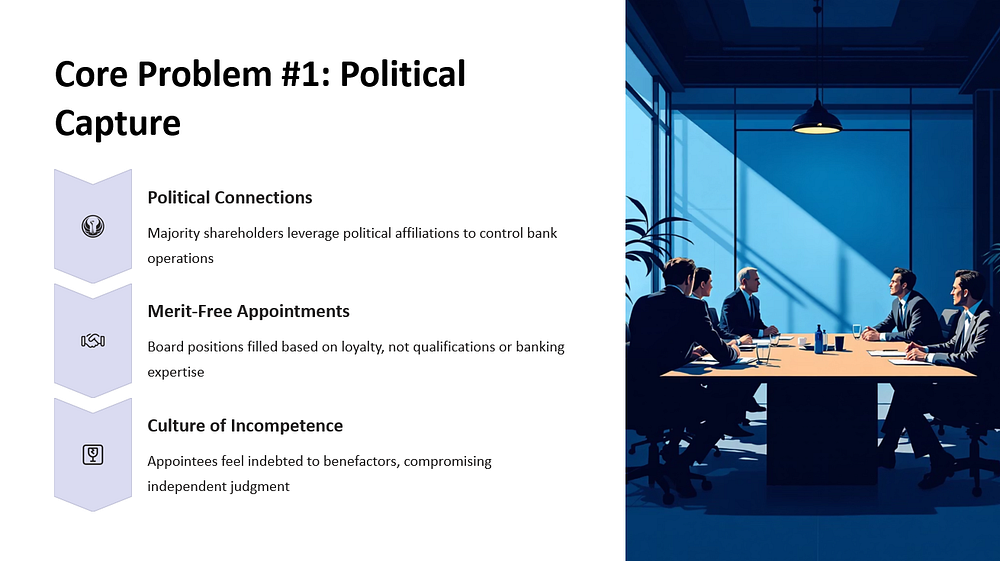

Political Interference

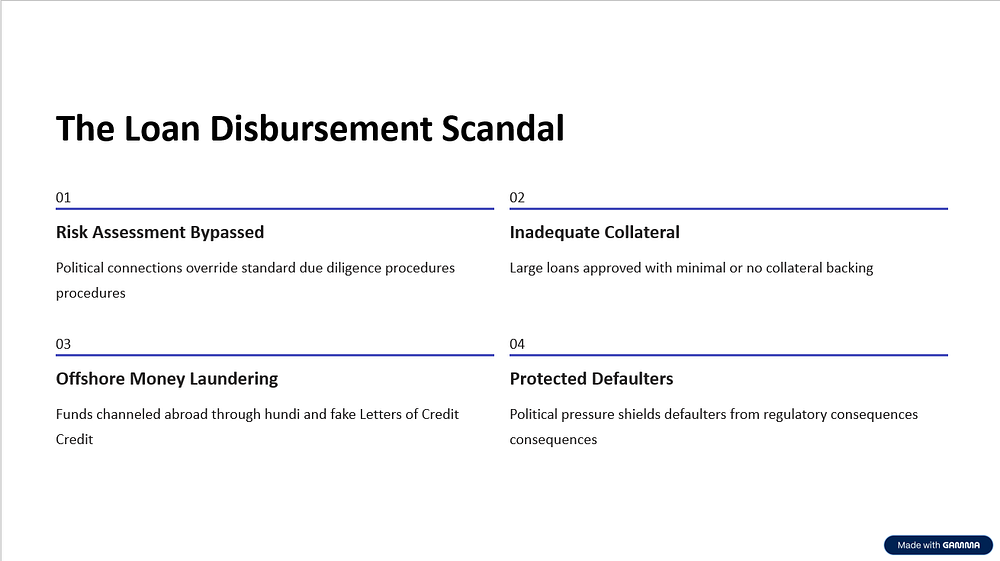

At the core of this current crisis is the unchecked influence of majority/ controlling shareholders. These shareholders have been unabashedly putting their favourites in all positions: starting from employees at all levels, even board of directors and chairperson. These appointments are done based on political affiliations or connections, not merit. This has created a culture of incompetence in running, and consequently ruining the banking sector, and has also created a sense of false or forced “fealty” among the appointees where they feel they “owe” something to their “benefactors” who secured their employment. This is particularly prevalent in disbursing loans to borrowers who neither have the intention nor the capacity to repay the loans if they went through a proper compliance test process before the loans were issued.

Large sums of funds are disbursed via loans to these politically connected individuals without adequate collateral or even no collateral at times, bypassing proper risk assessments. These loans often end up being laundered offshore via hundi or fake LC (Letter of Credit). When these loans end up being defaulted, the defaulters exert their political pressure on the regulators to look the other way or not take actions against the defaulters.

Family-Controlled Boards and Ignoring Conflicted Interests

Most banks are founded, or owned, or controlled by its founders, who treat the banks as their personal coffers. Their majority stakes entitle them to call the shots to fund their own business and/or personal interests and/or their friends and families. Instead of going public, which would make them accountable to its depositors, shareholders, and regulators, they prefer to remain private. These immoral practices erode the independence of the management as they have to give in to pressures or “requests” from the board even if they violate fundamental banking principles or give rise to clear conflict of interests. The very individuals tasked with ensuring good compliance, governance or risk management for the bank are the ones who end up being coerced into issuing bad loans which won’t ever be repaid.

Weak Transparency and Regulatory Oversight

The checks and balances that were supposed keep banking operations transparent have instead been compromised. Internally, compliance, governance & regulatory affairs teams are hamstrung by the influence of the board who are themselves “dependent”. Externally, on top of political influences, external auditors are “convinced” to balance the books to paint a portray a clean financial health report of banks while they are collapsing internally. Lately, it has been revealed that many banks which have been giving completely pristine audit reports were in fact on the brink of collapse.

Regulatory oversight is something most banks don’t take seriously. Their boards & political connections can stop any investigations on their tracks that the regulatory bodies initiate. Additionally, the so-called clean records generated by the façade of internal and external audit reports don’t really paint any major red flags of financial malpractice for the regulators to notice. The smaller minority shareholders lack control/influence over the board to voice their concerns or make any impactful complaints to the regulators.

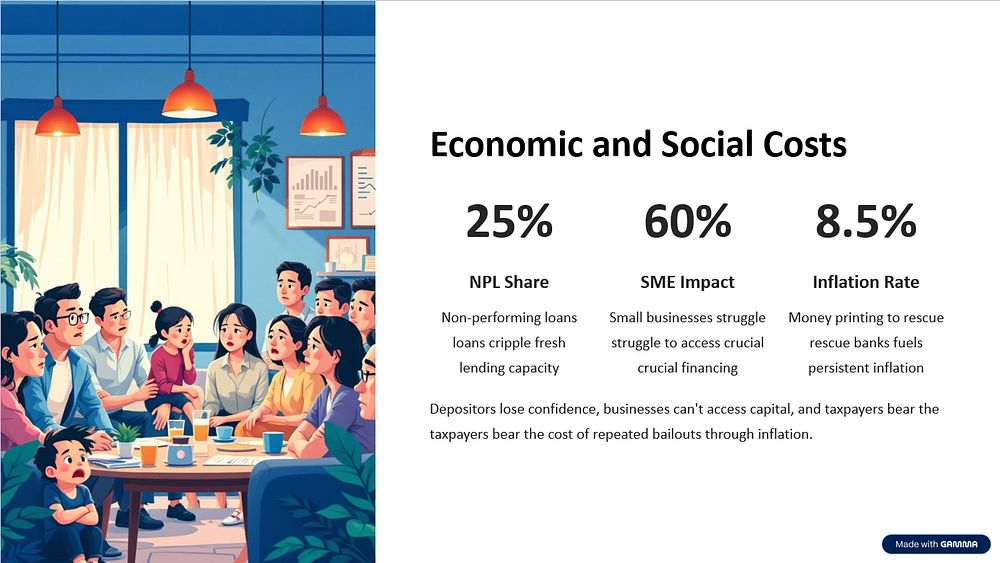

The Human and Economic Costs

The impact of these failures is not insulated from the wider economy. NPLs now account for a large share of the banking sector which stifles the flow of fresh funds towards profit generating businesses, reducing bank’s profitability. This also makes shareholders’ dividends uncertain. The backbone of our economy, the SME (Small to Medium Businesses) sector, is the worst affected by far.

Repeated financial scandals have also gravely impacted depositor confidence. Customers do not feel safe entrusting the banks with their hard-earned savings. The government’s response usually has been to print more money to inject these failing banks, rewarding this mismanagement culture instead of punishing them resulting in consistently high inflation — the price which is again paid by the public.

Rules won’t work without enforcement

The primary regulators for banks, the Bangladesh Bank has constantly issued timely circulars addressing these issues. However, Bangladesh Bank is not an enforcement body. Therefore, when they do try to take any actions, they are foiled by politically connected defaulters and family backed boards. Rules without enforcement do not mean much.

Recommendations for banking reforms addressing these issues

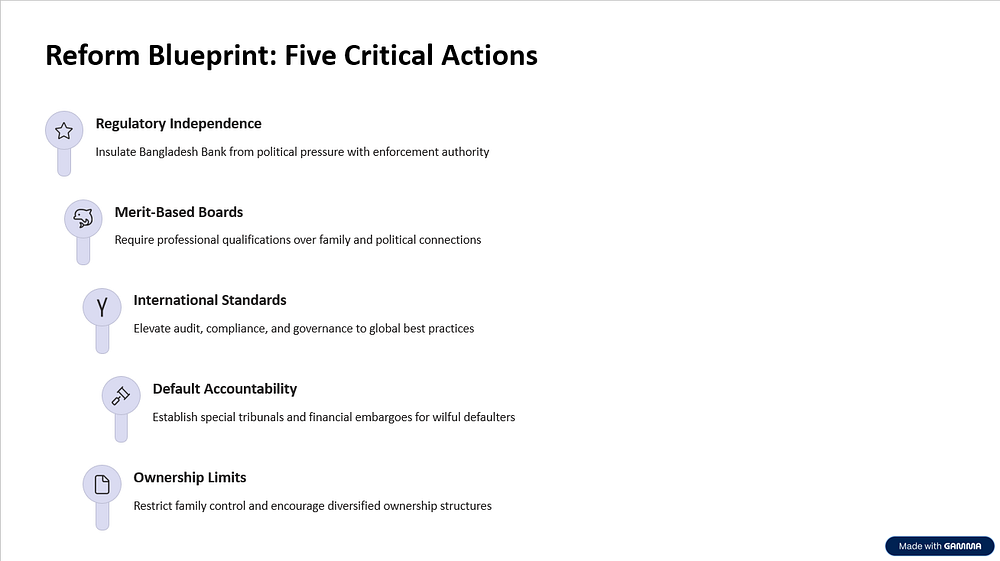

1. Ensuring Regulatory Independence

Bangladesh Bank must be allowed to be truly independent and self-governed by insulating its leadership away from political pressures. They must have the authority to penalize defaulters regardless of their affiliations, revoke or suspend financial licences or prevent/remove farcical appointments.

2. Bank Board reformation

Appointments to the boards should be based on merit and professional expertise, not political or family ties. A clear distinction is required between the ownership/majority shareholders of the bank with the management to reduce conflicts of interest. Additionally, Bangladesh Bank should have the ability to enforce them.

3. Strengthening Audit, Compliance, Governance and Transparency

Audit, Compliance & Governance standards have not worked clearly due to a lack of oversight, evident by NPLs that weren’t stopped from the start. Future standards should be of international standards and more importantly enforceable.

4. Tackling the culture of loan default normalisation

Loan defaulters, regardless of political or business influences must face legal consequences and financial embargoes instead of staying legal proceedings for years on end. A new standardized system of asset recovery, special speedy tribunals and restrictions/further financial scrutinization must be enforced on wilful defaulters to set an example to others who may attempt to abuse the current system.

5. Protecting Depositors and Shareholders

Protection of depositors must be ensured even if implementing these reforms mean dissolving some financial institutions. While current laws do have protection for minority shareholders, they can be improved.

6. Limiting Family and Group ownerships

Just as monopiles are bad for the economy, concentration of ownership in the palms of a few families are equally harmful, if not more. This culture has weakened governance. Regulators can set limits on family representations on boards and encourage diversified ownership structures.

Bangladesh cannot sustain its growth economically if our banking system remains feeble and compromised. The solutions are well known: independence, accountability, transparency, good compliance, governance, and professionalism. What’s missing is the willpower to enforce them.

Without reforms, banks shall continue to drain public resources and undermine investor & depositor confidence alike. With reform, banks can once again become huge engines of economic growth.

Written by

Shafqat Aziz

Barrister (of Lincoln’s Inn)

LLM Corporate Law, NTU

PGDL, UWE Bristol

LLB, BPP University

Accredited Civil-Commercial Mediator (ADR-ODR International)

Comments

Post a Comment