The Case for Expanding Bank Deposit Insurance in Bangladesh

Every day, news headlines highlight the precarious financial health of our local banks. Reports of looming bankruptcies often trace back to the growing burden of unrecoverable “bad loans”.

Simply put, bad loans are those loans which are unlikely to be repaid, either on time or at all. This creates a significant challenge for banks, as their core business relies on lending to individuals and businesses, expecting repayment of the principal along with interest within a set period. These funds are sourced from customer deposits to the bank for safekeeping or investment purposed. When borrowers default entirely, the financial stability of the banks is severely undermined, threatening the very foundation of their business model.

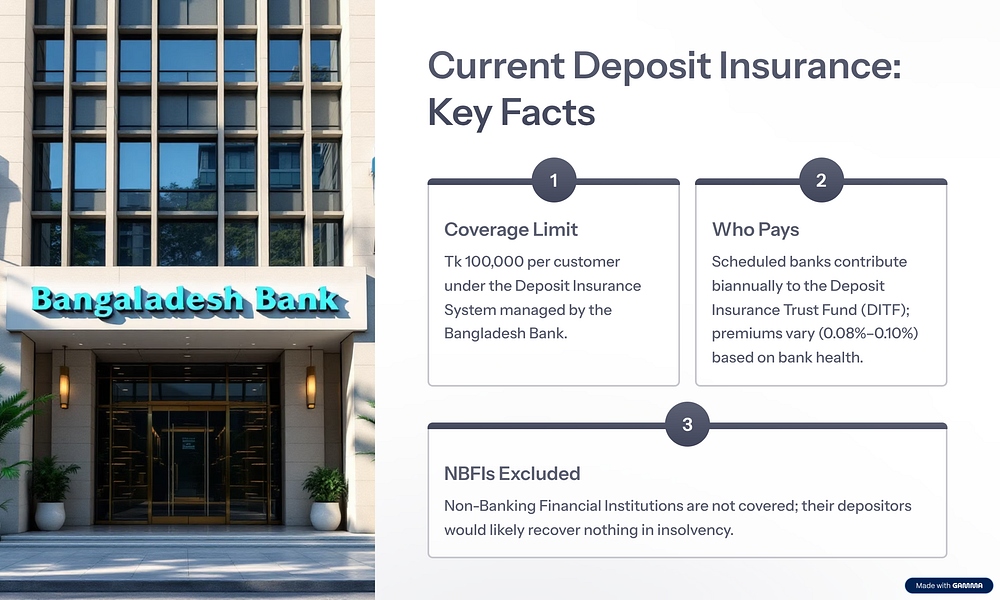

Currently, all scheduled bank deposits are insured by the Deposit Insurance System which is an initiative by the Bangladesh Bank to insure customer deposits up to BDT 100,000. This essentially means, if a bank becomes insolvent or bankrupt, customers may recover up to BDT 100,000 of their money regardless of how much money they had deposited into the bank.

For example, if X had BDT 500,000 in a bank which went bankrupt, X will only be entitled to recover BDT 100,000 out of the BDT 500,000 which was deposited into the bank by X.

However, once the bank is liquidated, whatever funds are recoverable will be used to pay off creditors and shareholders. After which, if any funds are remaining will be used to pay the remaining depositors on a proportionate basis based on their deposited amount.

Now would be a good time to clarify that NBFI (Non-Banking Financial Institutions) are not under the ambit of this scheme which essentially translate to NBFI customers losing all their deposits and not being able to recover anything if the NBFI goes bankrupt.

For the customers of a scheduled bank going bankrupt, this BDT 100,000 is paid to the customers out of the Deposit Insurance Trust Fund (DITF) which is managed by the Bangladesh Bank Trustee Board. This fund takes contributions from scheduled banks on a bi-annual basis based on their financial health. Basically, weaker the bank is financially, the more they have to pay per customer towards the DITF while the stronger a bank is financially, the less they have to pay per customer towards the DITF ranging from 0.08% 0.10% premium rate.

For most people, the meagre insurance sum of BDT 100,000 per customer is quite disappointing and this is even more relevant today as this scheme was enacted some two and a half decades ago.

Back then, in 2000 Bangladesh was an economy with a GDP of USD 67 Billion, in 2024 this has grown to a size of USD 450 Billion (even with conservative estimates, its around the USD 400 Billion ballpark currently).

Additionally, in the last 20 years, Bangladesh with a comparative young population enjoyed healthy average economic growth rate of 5–7% regardless of domestic or global macroeconomic instabilities. Pair this up with rampant corruption and uncontrolled inflation particularly since covid lockdowns, the value of the BDT has depreciated drastically reducing the value of our currency.

The insurance coverage of BDT 100,000 per customer is not only insufficient but also unfair, especially in an economic environment where many people are unable to withdraw their hard-earned money due to banks facing liquidity crises. This situation has fostered growing mistrust among the public toward local banks, which is alarming. Banks rely on customer deposits to issue loans and generate interest, which in turn funds their operations. However, the current lack of adequate safeguards undermines confidence in this system.

If we zoom out a bit, each scheduled banks are an integral part of the wider economy. Just one bank failing can cause ripple effects across a nation’s financial system. Imagine bank X which holds the deposits of just 100 customers for example, if bank X becomes bankrupt, it will stress the whole financial system directly and indirectly as a big chunk of funds will no lost from the financial system. Additionally, the customer’s deposits which they will lose beyond the BDT 100,000 insurance will more than likely not be recoverable which might have been better utilized if spent on goods and services within our economy as they would stimulate the economy via loans to SMEs. Lastly, these lost funds are also a loss to the government itself as they were taxable funds which are a source of fund for the NBR.

Expanding the Bank Deposit Insurance net would also be a good preventive measure to counter the risk of a bank run if any weak banks do end up going insolvent. A bank run is when all customers of a bank attempts to withdraw all their deposits in a short span of time.

This is something which may spread even more panic as most banks do not hold 100% of customer deposits at any given time due to the concept of fractional reserve banking. Fractional reserve banking is a concept whereby banks are required to hold only 10% of their cumulative customer deposits while the rest 90% can be utilized in providing loans and other investments. However, this is a tried and tested method and it is safe as because if the banks stopped doing this, the economy would slow down significantly.

The existing deposit insurance framework in Bangladesh, with its outdated coverage limit, no longer reflects the economic realities or the financial risks faced by depositors today. As the country’s economy has grown significantly over the past two and a half decades, so too has the volume of individual and institutional deposits. The existing insurance coverage undermines depositor confidence and threatens the stability of the financial system, especially in an era of increasing economic volatility.

Expanding the deposit insurance coverage is not just a protective measure for depositors but also a strategic move to bolster the banking sector’s resilience and people’s confidence in the financial system. It would reduce the likelihood of destabilizing bank runs, strengthen public trust in financial institutions, and ensure that customer deposits are safeguarded against unforeseen crises. Moreover, a robust insurance mechanism would contribute to economic growth by encouraging savings and fostering a more stable financial ecosystem.

As Bangladesh continues to develop, it is imperative to update existing financial safeguards to align with the economy’s growth trajectory. By increasing the deposit insurance limit and extending its scope to include Non-Banking Financial Institutions, the country can secure its financial future and ensure greater economic security for its citizens.

Written by

Shafqat Aziz

Barrister (of Lincoln’s Inn)

LLM Corporate Law, NTU

PGDL, UWE Bristol

LLB, BPP University

Accredited Civil-Commercial Mediator (ADR-ODR International)

First published by The Daily Star: The Case for Expanding Bank Deposit Insurance in Bangladesh

Comments

Post a Comment